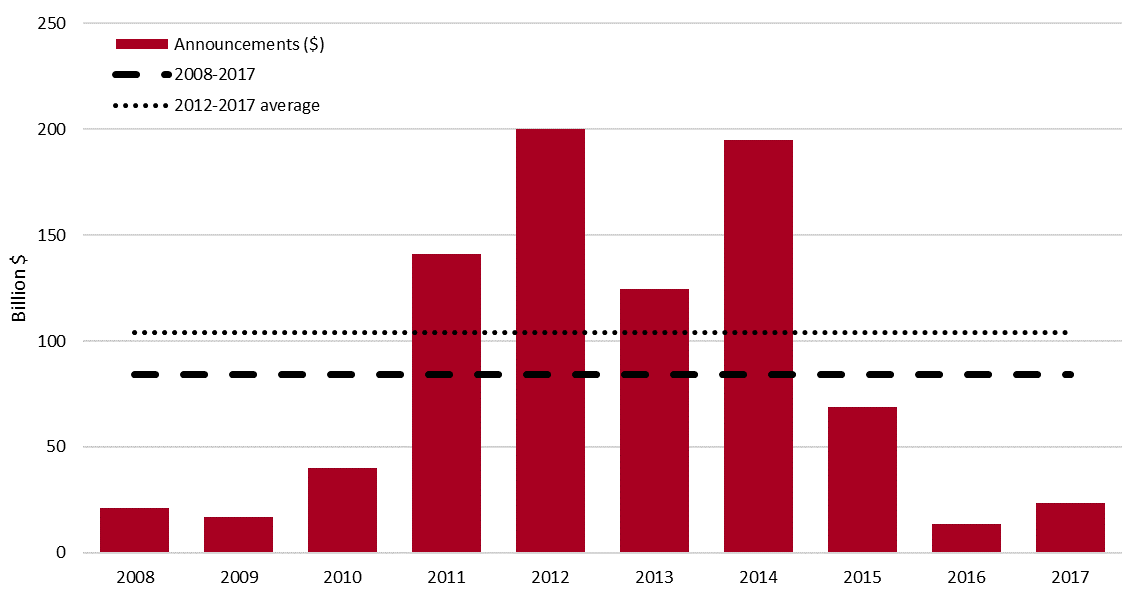

Natural Resources : the Rise of the Canadian InvestorFive years after the peak of the commodity boom, the investment climate has changed in Canada. Activity has slowed, the dust has settled, and the new landscape of natural resource industries is now more visible. Foreign investors appear to be spooked by Canadian infrastructure bottlenecks and some are probably lured by the new regulatory and fiscal easing south of the border. Foreign investors: in free fall Industrial investment in Canada, as determined based on investment announcements, shows a sharp drop in foreign direct investment—and more specifically, in capital expenditures. In fact, foreign investment in Canada in 2017 was 10% of the peak level of 2013 in the industrial sectors. New Industrial Megaprojects – Canada – 2008 to 2017 Source: E&B DATA, CAPEX-Online, 2017. Based on project announcements.

While new large-scale investments are apparently at recessionary levels1, the situation is far from negative for investors who have successfully completed their projects.

After the period of robust growth in resource-industry production capacity since the beginning of the decade, resource industries in Canada are now limiting capital expenditures and raking in profits. Some projects are emerging but will move ahead only once the medium-term economic outlook has stabilized. Overall, the period saw the rise of a major Canadian-owned resource industry, which is here to stay. Even without having access to the same financing and marketing networks as their major international competitors, Canadian investors continue to thrive in an institutional, regulatory and competitive environment that is certainly more restrictive than in some competing regions. In fact, Canadian investors are regaining a dominant share, with nearly 80% of the value of the megaprojects emerging in Canada over the next decade3). ******

[1] Most of the data in this economic note can be found in “Foreign Investors Running for the Exit” – Megaprojects Outlook – Canada. March 2018. E&B DATA.↑

[2] Source: But where are the investors? March 2018. E&B DATA.↑ [3] Source : CAPEX-online. E&B DATA.↑

|

E&B Data

Economic and Business Data