The End of the Great Era of Industrial Megaprojects: Taking Stock

Though more than $700 billion in megaprojects have been announced in Canada, almost all in the natural resources sector, over half that amount is at risk1. In terms of geopolitics relating to commodities, Canada has been severely shaken but is not out of the game, by far. Despite the current quasi-deflationary situation for commodity prices and amid a de facto currency war, not all Canadian commodity producers are on the losing side.

Exporters: 1, investors: 0

Even though investment in the oil and minerals sectors is plummeting, new production capacities commissioned in Canada in recent years have contributed to record export levels, in spite of the widespread international price decrease.

Oil: OPEC production policies, especially in Saudi Arabia, explicitly aim to chase out high-cost crude producers. As a result, Canadian investors are indeed in bad shape, with nearly $170 billion of announced projects suspended or pending abandonment. However, investment activity has not completely stopped, as large-scale projects are notoriously difficult to stop once construction has begun2. After all, the overall profitability of these long-term projects (with a lifespan exceeding 30 years in most cases) can generally endure a downturn, even if it lasts a few years. But this resilience is not endless, and since no significant price increase is expected in the short term3, the most fragile producers will soon be forced into precipitated asset sales. That said, Canadian extraction activity is in full swing and production volume has reached historic highs (nearly four million barrels per day of crude oil4).

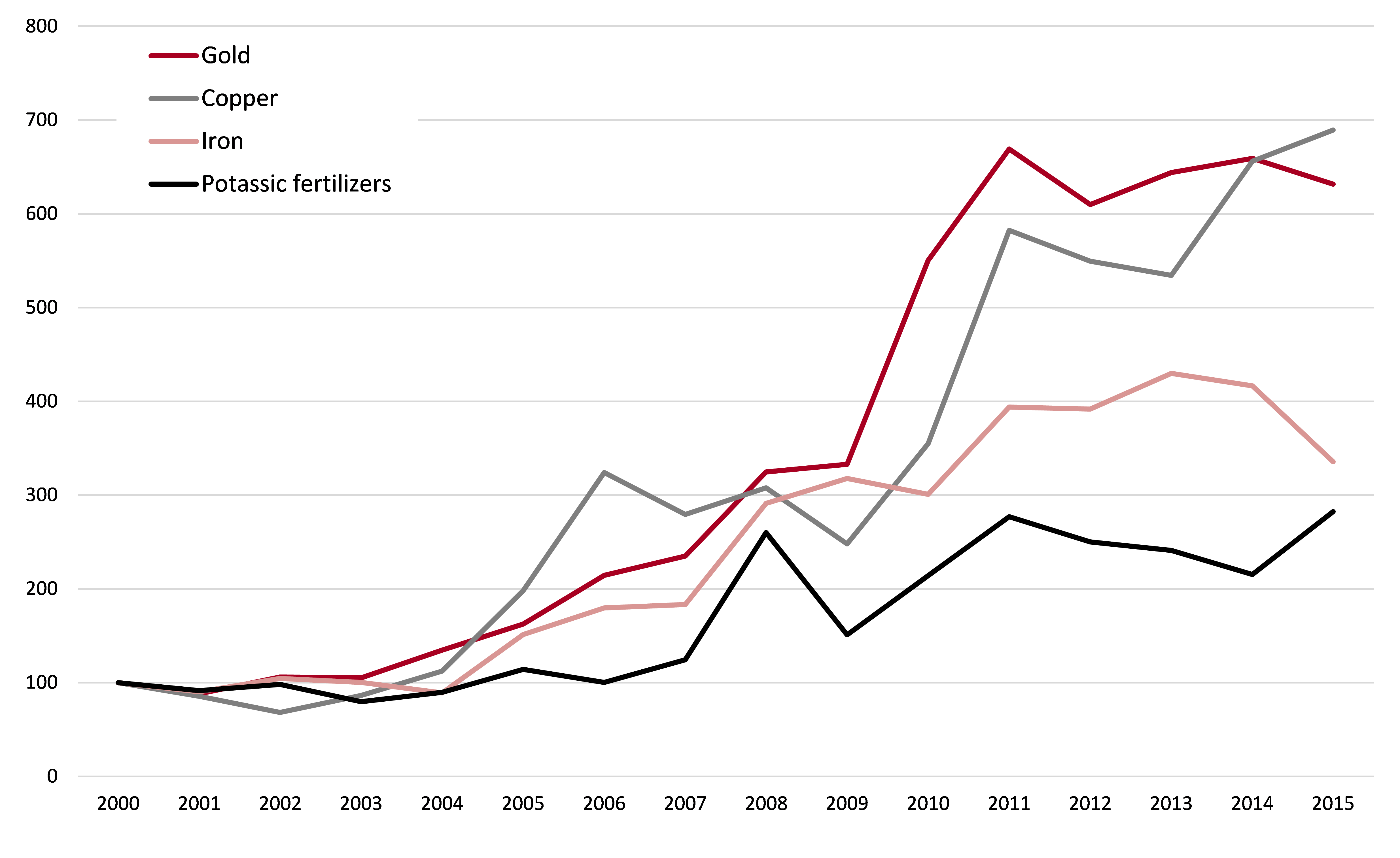

Minerals: While most announced megaprojects have been suspended, megaprojects that were commissioned in recent years (e.g. ArcelorMittal at Mont Wright, QC, and PotashCorp at Rocanville, SK) are now in their production phase. This explains the substantial rise in the total value of exported minerals (increased by a factor of three between 2000 and 2015), which has been holding steady since 2011 despite falling commodity prices5. For minerals with the largest export values, levels remain high compared to the last decade and have sometimes even reached record peaks.

Mineral/Metal Selection – Export value – Canada – Base 100 = 2000 – 2000 to 2015

Source: Industry Canada.

The drop in prices of minerals is offset by a lower Canadian dollar, while the impact on profitability is mitigated by lower fuel prices. However, this unfavorable environment for new investors in Canada (high cost of machinery imports) is more beneficial for companies that refrain from large-scale investing and focus on their operations. With the realignment of Canadian and US dollars, many Canadian exporters appear to be profiting from the situation.

Missed opportunities?

Natural gas: Canada’s window of opportunity for establishing a new liquefied natural gas terminal industry is closing (over 20 projects worth nearly $285 billion). No project has reached the construction stage and virtually none of them has a chance to be commissioned before 20206, while 11 competing projects in the United States and Australia are already under construction7 and are favoured to serve the Asian market. Will Canada be in a better position to reach the European market, helping to reduce European dependence on Russian gas? If so, some projected terminals on the East Coast (e.g. Repsol Canada in Saint John, NB, or Pieridae Energy in Goldboro, NS) could benefit from this new geostrategic alignment. Will they be ready in time?

Slow and steady wins the race

Recently completed large industrial capacities are enjoying a relatively advantageous position. For those still at the project stage, it might already be too late…

[1]“End of the Great Era of Industrial Megaprojects”. Megaprojects Outlook. E&B DATA. February 2016. [2] Their high degree of inertia is explained by the large costs of abandonment (and site decommissioning), shutdown and operation restart, not to mention the importance placed on sunk costs. [3] In part because of unusually high inventories that could take years to reduce thereby extending the surplus of supply over demand and the downward pressure on prices. See: Bloomberg Business, “Shale Oil Isn’t Saudi Arabia’s Only Nemesis”, March 1, 2016. [4] Four per cent of world production. National Energy Board (NEB) and the Canadian Association of Petroleum Producers (CAPP). [5] Statistics Canada, Table 228-0059. [6] E&B DATA, CAPEX-Online, 2015. [7] Four projects under construction in the U.S. and seven more in Australia. Source: International Gas Union, “World LNG Report – 2015 Edition.” The Sabine Pass megaproject in Louisiana (Cheniere Energy) is the first LNG export terminal in North America to be commissioned (first quarter 2016).